Sustainability Reporting

Europe on the path to becoming the first climate-neutral continent: The EU Green Deal

Through the European Green Deal, the countries of the European Union have set themselves the goal of making Europe the first climate-neutral continent by 2050. To achieve this goal, net greenhouse gas emissions are to be reduced by at least 55% by 2030 (compared to 1990). As a further interim target, the European Commission has set a greenhouse gas reduction of 90% by 2040 (compared to 1990).

The measures set out by the EU to achieve these targets include, amongst others:

- Legislative changes such as the European Climate Law, which makes the net-zero target binding, or various disclosure directives and regulations (including CSRD, EU Taxonomy, SFDR, CSDDD, EmpCo) for companies to ensure transparency

- Funding, particularly for clean investments, climate protection measures, economic diversification, energy efficiency, disaster risk reduction and renewable energy

- An EU Emissions Trading System and a Carbon Border Adjustment Mechanism to ensure appropriate carbon pricing

- Objectives promoting the circular economy, for example regarding the management of critical raw materials, the reduction of pollutants, sustainable packaging, the ban on the destruction of unsold goods, and the design of products to be repairable

Reporting of sustainability information plays a bigger role in law under the EU Green Deal

The growing number of legal changes regarding disclosure requirements presents one of the biggest hurdles for companies, as they must simultaneously deal with the issue of sustainability and the associated obligations. Although reporting obligations such as the NFRD (Non-Financial Reporting Directive) already existed, these have been expanded since the announcement of the EU Green Deal at the end of 2019. The following disclosure requirements are among the best known, although their content and scope have changed in some respects since the so-called Sustainability Omnibus:

- CSRD – Corporate Sustainability Reporting Directive

This directive, which has already entered into force, requires companies in the EU with 1,000 or more employees and an annual turnover of 450 million euros or more to prepare an audited sustainability statement in accordance with the EU Standard for Sustainability Reporting, the ESRS or European Sustainability Reporting Standards.

- EU-TAX – EU Taxonomy Regulation

This regulation, which has also already entered into force, applies to the same companies as the CSRD. When preparing their sustainability statement, these companies must assess their economic performance (covering both revenue and expenditure) in terms of environmental sustainability using the EU Taxonomy classification system.

- SFDR – Sustainable Finance Disclosure Regulation

This directive, which is also already in force, requires financial market participants and advisers to disclose sustainability-related information on investments based on ESG factors.

- CSDDD – Corporate Sustainability Due Diligence Directive

This directive requires companies in the EU with 5,000 or more employees and an annual turnover of €1.5 billion or more to fulfil sustainability-related due diligence obligations within their supply chain. The CSDDD comes into force on 26 July 2029.

- EmpCo – Empowering Consumers for the Green Transition

This directive replaces the so-called Green Claims Directive and must be complied with from 27 September 2026 in all EU Member States by companies offering products and services in the EU. The B2B market is also affected, if end consumers receive communications from these companies. Greenwashing is to be minimised by subjecting environmental claims to stricter regulation under the EmpCo.

How companies should approach the reporting requirements under the EU Green Deal

The new regulations mean that, for an increasing number of companies, addressing the environmental and social impacts of their own business activities is no longer merely optional, but is becoming crucial to business success.

However, there are areas where companies do have significant influence:

- How they communicate on sustainability and how efficiently they collect and subsequently maintain the necessary data and information

- The extent to which they incorporate sustainability factors into their business decisions

A sustainability strategy can effectively support companies in both above areas and provide significant competitive advantages through

- Robustness of the business model

- Advantages in fundraising

- Greater attractiveness as an employer

- Improved evaluation as a supplier

- Proactive management of sustainability opportunities and risks throughout the entire value chain

- Targeted sustainable product innovations

The EFS Consulting service portfolio for Sustainability Reporting

EFS Consulting supports and develops sustainability projects of all kinds – from the initial exploratory phase right through to the implementation of a company-specific sustainability strategy.

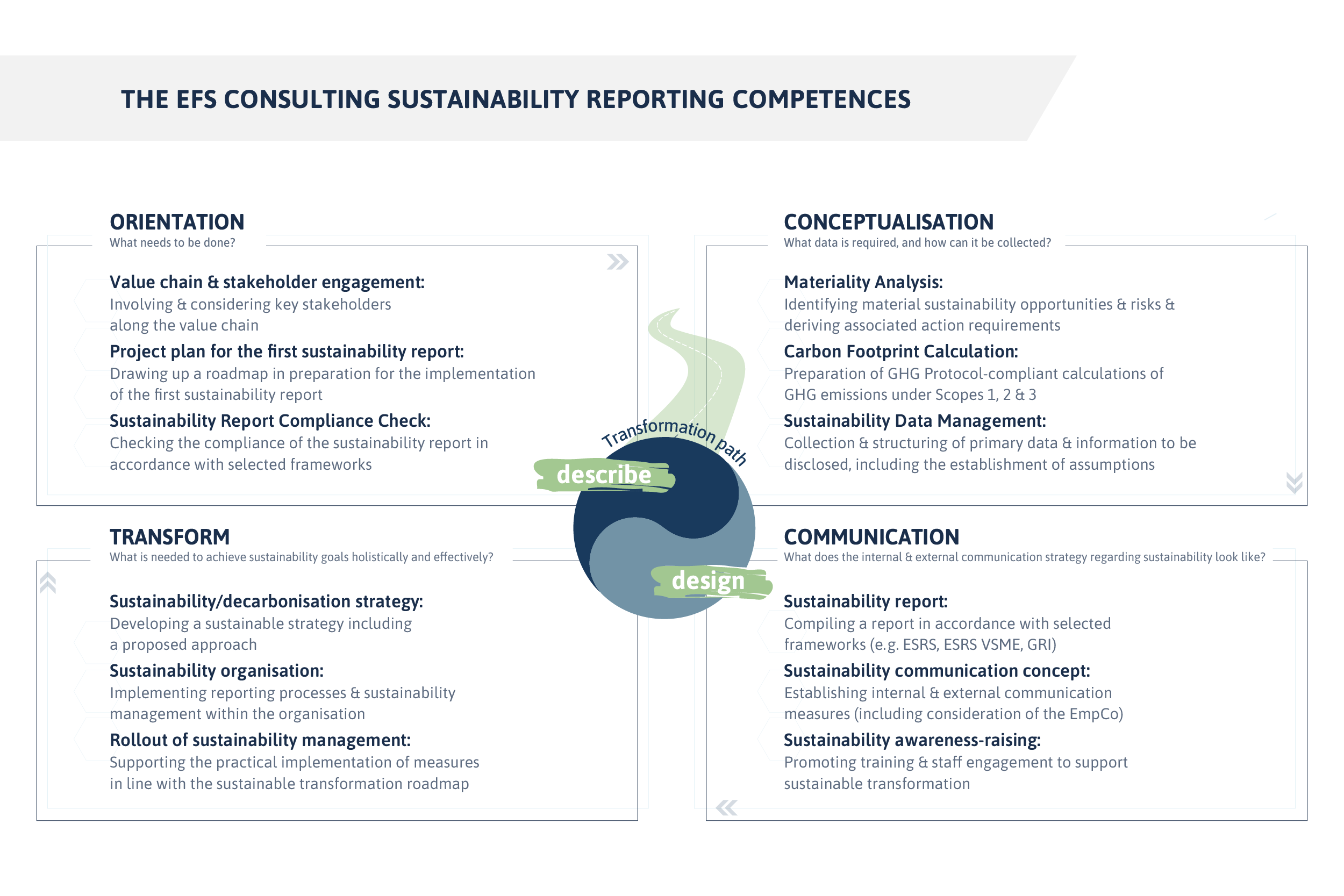

4 chapters of the Sustainability Reporting service portfolio

Orientation – What needs to be done?

- Value chain and stakeholder engagement: Involving and considering key stakeholders along the value chain

- Project plan for the first sustainability report: Drawing up a roadmap in preparation for the implementation of the first sustainability report

- Sustainability Report Compliance Check: Checking the compliance of the sustainability report in accordance with selected frameworks

Conceptualisation – What data is required, and how can it be collected?

- Materiality Analysis: Identifying material sustainability opportunities and risks and deriving associated action requirements

- Carbon Footprint Calculation: Preparation of GHG Protocol-compliant calculations of GHG emissions under Scopes 1, 2 and 3

- Sustainability Data Management: Collection and structuring of primary data and information to be disclosed, including the establishment of assumptions

Communication – What does the internal and external communication strategy regarding sustainability look like?

- Sustainability report: Compiling a report in accordance with selected frameworks (e.g. ESRS, ESRS VSME, GRI)

- Sustainability communication concept: Establishing internal and external communication measures (including consideration of the EmpCo)

- Sustainability awareness-raising: Promoting training and staff engagement to support sustainable transformation

Transform – What is needed to achieve sustainability goals holistically and effectively?

- Sustainability/decarbonisation strategy: Developing a sustainable strategy including a proposed approach

- Sustainability organisation: Implementing reporting processes and sustainability management within the organisation

- Rollout of sustainability management: Supporting the practical implementation of measures in line with the sustainable transformation roadmap